Tax year is the calendar year but may be shorter than 12 months where activities start or terminate during a calendar year or there is a change in the status of the entity.

A legal entity is considered resident if it is incorporated in Serbia or managed or controlled from Serbia. Resident entities are taxed on their worldwide income; non-residents are taxed only on income generated in Serbia. The taxable base is calculated in the tax balance sheet, based on the profit and loss account adjusted for tax purposes. Taxable income includes both business income and capital gains. |

|

Tax filling in Serbia is based on self-assessment. Advance corporate tax is payable in monthly installments. A tax return and tax balance must be filled within 180 days after the end of the tax period for which the tax return is filled or 15 days from the deadline for submission of financial statements in case of a change of status, bankruptcy or liquidation.

Tax |

Rate |

Recurrence |

Possible Incentive |

| Corporate Profit Tax |

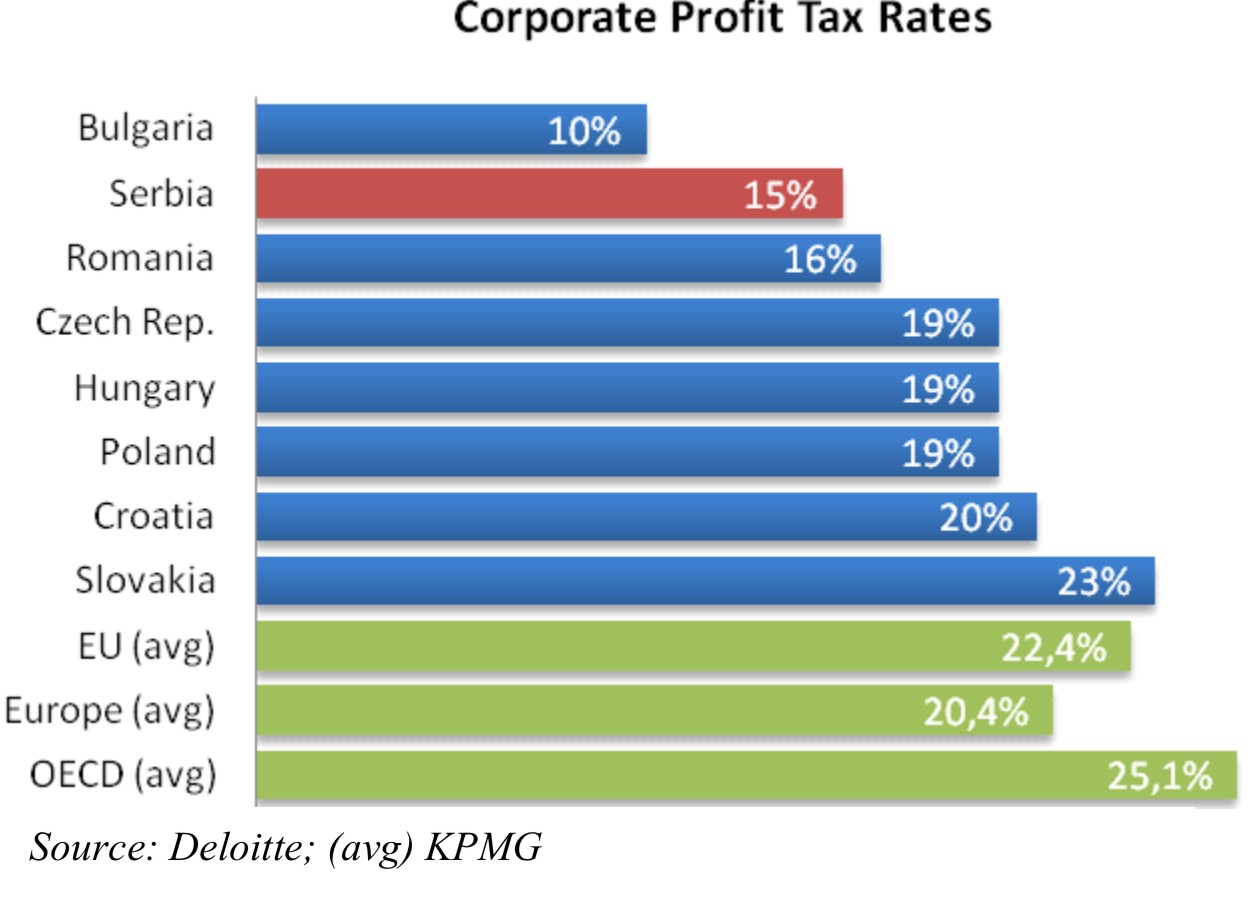

15% |

yearly |

10 year tax holiday

(investments in fixed assets over EUR 9 million and minimum 200 new jobs)

&

20% or 40% of investment value as tax credit |

| Withholding Tax (for dividends, royalties, interest income, lease payments for movable or immovable property) |

20% |

yearly |

lower rate according to Double Taxation Agreement |

Payments of dividends, interests, royalties, income from the lease of property and payments made for services provided by entities resident in preferential tax jurisdictions are subject to 20% withholding tax. Technical services fees and branch remittance tax are not subject to withholding tax.

Capital gains

Capital gains are subject to a 15% tax for residents (included in the annual income tax return) and 25% for non-residents (based on the tax assessment) unless the rate is reduced under a tax treaty.

Taxation of Dividends

Dividends paid by a Serbian resident company to another Serbian company are exempt from corporate income tax. Dividends received by a Serbian resident company holding at least 10% of the shares in a non-resident representative office are eligible for a credit for foreign tax paid on the dividends.

Anti-Avoidance Rules

Transfer pricing – transactions between associated entities must be on arm’s length terms.

Under the thin capitalization rules, interest and related expenses are deductible on loans that do not exceed taxpayer’s equity 4 times for companies and 10 times for banks. In addition, under the transfer pricing rules a taxpayer must demonstrate that interest that is deductible under the thin capitalization rules is at an arm’s length level. Otherwise, an adjustment of taxable income may be required.

Companies are considered related if one company has the ability to control or influence the business decisions of the other company or if a company holds at least 25% of the shares or votes in the governing body of the other company.

Additional Information

Resident company may elect for group status and file a consolidated return. Companies are considered a group where parent company owns at least 75% of the shares or stocks of another company. The parent company file a consolidated tax return in which gains and losses of group companies are offset and each company pays its share of the tax. Once initiated, tax consolidation must be applied for 5 years.

Deductibility of marketing expenses is capped at 10% of gross revenue. Entertainment expenses are treated separately and are deductible up to the limit of 0.5% of gross revenues.

Stamp duty is payable according to a tariff based on the value of the document. If there is no value, a flat rate applies.

Real property tax is levied on immovable property located in Serbia at 0.4% rate of book value.

For transfer of property (e.g. real property, intellectual property, etc.) a 2.5% tax rate applies.

Value Added Tax

VAT is imposed on the provisions of goods and services. The lower rate of 8% is for basic food, daily newspapers, utilities, etc.

The registration threshold for VAT purposes is an annual turnover of RSD 8 million.

VAT taxpayers with taxable income above RSD 50 mil are required to file monthly VAT returns within 15 days after the end of the tax period and pay the difference between the amount specified in the tax return and the input VAT incurred. VAT taxpayers with taxable income below RSD 50 mil must file quarterly VAT returns within 20 days after the end of the tax period. |

|

Refund period is 45 days (for major exporters 15 days).

Non-residents are not allowed to deduct input VAT through fiscal representatives.

Tax |

Rate |

Recurrence |

Possible Incentive |

| VAT |

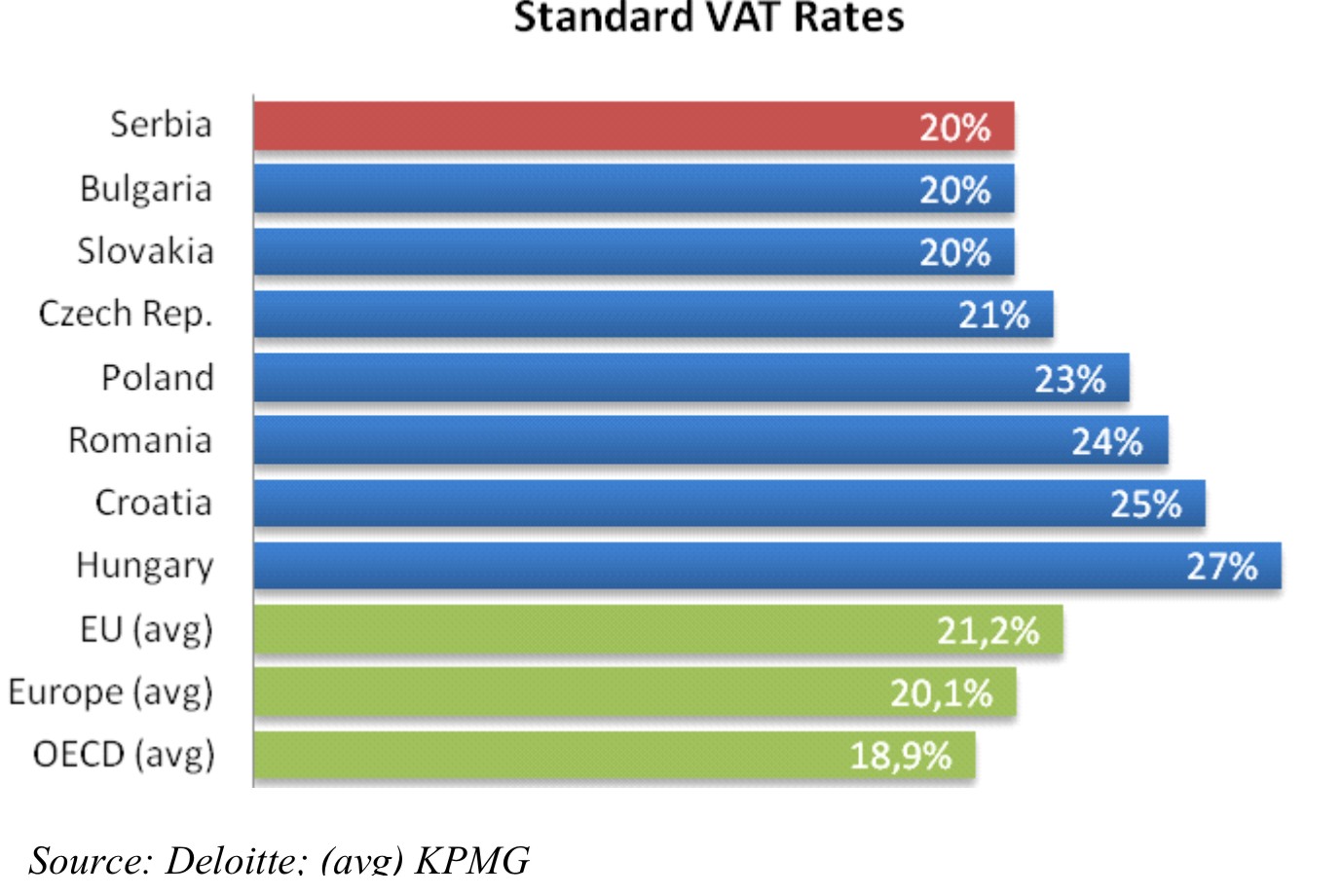

20% - standard

8% - lower

|

monthly |

import VAT return for export of finished goods

import VAT exempt in free trade zones

|

INDIVIDUAL TAXATION Basis

Serbian residents are taxed on their worldwide income; non-residents are taxed only on income generated in Serbia. For income tax purposes, an individual is considered resident if he/she has a residence or center of business or stays in Serbia for at least 183 days in the total during the tax year.

Tax |

Rate |

Recurrence |

Possible Incentive |

| Salary Tax |

10% |

monthly |

3 - year holiday for hiring apprentices

2 - year holiday for hiring unemployed workers

|

| Annual Income Tax |

10% - 3x-6x average salary

15% - over 6x average salary

|

yearly |

|

The principal taxable forms of income are employment income (10%), business income (10%), royalties and rent, (20%) and capital gains (15%). Residents receiving income of 3 or more times the annual average earnings in the tax year are subject to annual income tax under the worldwide system.

Total costs for employers stand at merely 50% of the level in EU countries from Eastern Europe. Social insurance charges and Salary Tax amount to roughly 65% of the net salary but the tax burden for employers can be reduced through a variety of financial and tax incentives available.

Mandatory Social Security Contributions

(Recurrence - Monthly) |

On Behalf of

Employer |

On Behalf of

Employee |

| Pension and disability insurance |

11% |

13% |

| Health insurance |

6.15% |

6.15% |

| Unemployment insurance |

0.75% |

0.75% |

Non-taxable income threshold is RSD 11,000 (app. EUR 96). Salary tax is paid under the PAYE system, whereby tax is deducted at source by the employer. Other income is self-assessed. Individuals must file a tax return or pay withholding tax depending on the type of income. Spouses are taxed separately.

The rates dues by the self-employed are 22% for Pension and disability insurance, 12.3% for Health insurance and 1.5% for Unemployment insurance. Pension and disability insurance SSC rate related to other types of personal income (eg. Service Agreement) is 24%.

Other Taxes on Individuals

Inheritance tax is levied on inheritances and gifts at progressive rate between 1.5% (for taxpayers in the second order of succession) and 2.5% (for taxpayers in the third and subsequent orders of succession).

Transfer tax of 2.5% applies on transfer of immovable property (i.e. intellectual property, real property, etc).

Property tax is levied on the occupation of real estate at progressive rates ranging from 0.4% to 2%..

If a taxpayer earns profit by conducting business in another country and tax was paid on that profit, one is entitled to a tax credit on its company profit tax account in Serbia amounting to the already paid tax. A taxpayer who earns revenue enjoys the same right and pays personal income tax in another country, provided there is a Double Taxation Treaty with that country.

Double Taxation Agreements (DTA) Signed by Serbia |

Albania |

Bulgaria |

DPR Korea |

Ghana* |

India |

Latvia |

Moldova |

Poland |

Spain |

Ukraine |

Austria |

Canada |

Denmark |

Georgia |

Indonesia* |

Libya |

Montenegro |

Qatar |

Sri Lanka |

UAE* |

Azerbaijan |

China |

Egypt |

Germany |

Italy |

Lithuania |

Netherlands |

Romania |

Sweden |

UK |

Belgium |

Croatia |

Estonia |

Greece |

Iran |

Macedonia |

Norway |

Russia |

Switzerland |

Zimbabwe* |

Belorussia |

Cyprus |

Finland |

Guinea* |

Ireland |

Malaysia |

Pakistan |

Slovakia |

Tunisia* |

|

Bosnia & Herzegovina |

Czech Republic |

France |

Hungary |

Kuwait |

Malta |

Philippines* |

Slovenia |

Turkey |

|

*Signed, to be confirmed by Parliament

DTA’s with Botswana, Vietnam, Zambia, Armenia, Jordan, South Africa and Morocco are initialled, while negotiations are under way with Luxembourg, North Korea, Myanmar Union, Nigeria and Syria.